MCLEAN, VA--(Marketwired - Dec 17, 2015) - Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing fixed mortgage rates ticking slightly higher for the second week in a row amid the Federal Reserve's decision to raise short-term interest rates for the first time since 2006.

MCLEAN, VA--(Marketwired - Dec 17, 2015) - Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing fixed mortgage rates ticking slightly higher for the second week in a row amid the Federal Reserve's decision to raise short-term interest rates for the first time since 2006.

News Facts

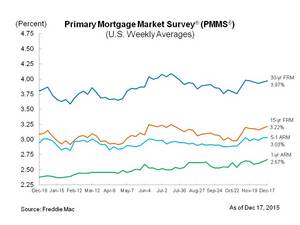

- 30-year fixed-rate mortgage (FRM) averaged 3.97 percent with an average 0.6 point for the week ending December 17, 2015, up from last week when it averaged 3.95 percent. A year ago at this time, the 30-year FRM averaged 3.80 percent.

- 15-year FRM this week averaged 3.22 percent with an average 0.5 point, up from last week when it averaged 3.19 percent. A year ago at this time, the 15-year FRM averaged 3.09 percent.

- 5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.03 percent this week with an average 0.4 point, unchanged from last week. A year ago, the 5-year ARM averaged 2.95 percent.

- 1-year Treasury-indexed ARM averaged 2.67 percent this week with an average 0.2 point, up from 2.64 percent last week. At this time last year, the 1-year ARM averaged 2.38 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following links for the Regional and National Mortgage Rate Details and Definitions. Borrowers may still pay closing costs which are not included in the survey.

As of January 1, 2016, the PMMS will no longer provide results for the 1-year ARM. Additionally, the regional breakouts will not be provided for the 30-year and 15-year fixed rate mortgages, and the

5/1 Hybrid ARM.

Quote

Attributed to Sean Becketti, chief economist, Freddie Mac.

"As was almost-universally expected, the Federal Open Market Committee (FOMC) of the Federal Reserve elected this week to raise short-term interest rates for the first time since 2006. We take the Fed at its word that monetary tightening in 2016 will be gradual, and we expect only a modest increase in longer-term rates. Mortgage rates will tick higher but remain at historically low levels in 2016. Home sales will remain strong, but refinance activity should cool somewhat. Novel policy approaches such as quantitative easing injected significant liquidity in the economy over the past seven years. As a result, the Fed is forced to employ some new tools, such as reverse repos, as it tightens monetary policy. We are likely to see some short-term volatility in fixed-income markets as market participants adjust to these new tools."

Freddie Mac was established by Congress in 1970 to provide liquidity, stability and affordability to the nation's residential mortgage markets. Freddie Mac supports communities across the nation by providing mortgage capital to lenders. Today Freddie Mac is making home possible for one in four home borrowers and is one of the largest sources of financing for multifamily housing. Additional information is available at FreddieMac.com, Twitter @FreddieMac and Freddie Mac's blog FreddieMac.com/blog.

The financial and other information contained in the documents that may be accessed on this page speaks only as of the date of those documents. The information could be out of date and no longer accurate. Freddie Mac does not undertake an obligation, and disclaims any duty, to update any of the information in those documents. Freddie Mac's future performance, including financial performance, is subject to various risks and uncertainties that could cause actual results to differ materially from expectations. The factors that could affect the company's future results are discussed more fully in our reports filed with the SEC.