MCLEAN, VA--(Marketwired - Aug 31, 2015) - Freddie Mac (OTCQB: FMCC) released today its monthly Insight & Outlook for August, showing there is no single statistic that reliably identifies when a housing market is overvalued or when house prices are likely to fall. Instead, substantial human judgment is also required. A video preview, along with the complete Insight & Outlook commentary is available here.

MCLEAN, VA--(Marketwired - Aug 31, 2015) - Freddie Mac (OTCQB: FMCC) released today its monthly Insight & Outlook for August, showing there is no single statistic that reliably identifies when a housing market is overvalued or when house prices are likely to fall. Instead, substantial human judgment is also required. A video preview, along with the complete Insight & Outlook commentary is available here.

Insight Highlights

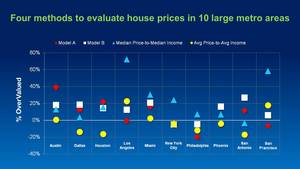

- The affordability metrics produced by the housing industry can indicate when prices are high relative to historical norms and to household income, but they cannot reliably predict if or when house prices in a particular market -- or the nation as a whole -- will fall.

- There is a surprising amount of disagreement among the various measures of overvaluation. The same metro area may be tagged as overvalued by one metric and undervalued by another measure.

- The future path of house prices is an important factor in measuring the credit risk -- and thus setting an appropriate guarantee fee -- of the mortgages that Freddie Mac funds.

- Freddie Mac has an important advantage over local lenders and homeowners by funding houses throughout the U.S. Isolated local house price declines are averaged in with house price increases in the rest of the country. As a result, the collection of loans funded by Freddie Mac experiences the average change of house prices nationwide.

- Of course, this diversification can't protect Freddie Mac against another national house price bubble. Instead, the various reforms in industry practice and regulation over the last seven years provide the defense against a repeat of that experience.

Outlook Highlights

- Due to stronger-than-expected refinance activity and home sales, estimate of 2015 mortgage originations have been increased to $1.45 trillion and 2016 originations to $1.3 trillion.

- Increased projection of 2015 home sales to 5.73 million units, which would be the best year since 2007.

- Revised 2015 refinance share up to 46 percent of all single-family mortgage originations.

Second Quarter 2015 Refinance Highlights

- Cash-out refinances increased from 27 percent of refinances in the first quarter of this year to 34 percent in the second quarter. A year ago, the cash-out share was 22 percent. During the housing boom, the cash-out share peaked at 89 percent in the third quarter of 2006.

- An increasing share of refinancing borrowers chose to shorten their loan terms. Of borrowers who paid off a 30-year fixed-rate loan in the second quarter, 40 percent chose a 15-or 20-year loan, compared to 39 percent in the first quarter.

Quote: Attributed to Sean Becketti, Chief Economist, Freddie Mac.

"Statistics by themselves cannot tell us whether housing in a particular market -- or the nation as a whole -- is overvalued. At best, affordability statistics wake us up to potential danger. In this way, they are like the signs posted every summer in national parks that indicate the current danger of a forest fire. We recognize when the danger is elevated, but we can't predict for sure if or when someone will accidentally drop a match in the wrong spot."

"In this month's Insight & Outlook, we also revisited the topic of low down payment mortgage programs -- like Freddie Mac's Home Possible Advantage -- that expand affordability for creditworthy borrowers. We compared actual losses on low down payment loans to losses on 20-percent down payment loans over the 10-year period 2003-2013, a period that includes the housing crisis. 30-year fixed rate loans with 3 percent down payments were only 17 percent riskier than 20-percent down payment loans over that period. As a comparison, 7/1 ARMs were 155 percent riskier than 30-year fixed rate mortgages over the same period, and 5/1 ARMs were five times as risky."

Freddie Mac was established by Congress in 1970 to provide liquidity, stability and affordability to the nation's residential mortgage markets. Freddie Mac supports communities across the nation by providing mortgage capital to lenders. Today Freddie Mac is making home possible for one in four home borrowers and is one of the largest sources of financing for multifamily housing. Additional information is available at FreddieMac.com, Twitter @FreddieMac and Freddie Mac's blog FreddieMac.com/blog.

The financial and other information contained in the documents that may be accessed on this page speaks only as of the date of those documents. The information could be out of date and no longer accurate. Freddie Mac does not undertake an obligation, and disclaims any duty, to update any of the information in those documents. Freddie Mac's future performance, including financial performance, is subject to various risks and uncertainties that could cause actual results to differ materially from expectations. The factors that could affect the company's future results are discussed more fully in our reports filed with the SEC.